I am a 33-year-old NRI and intend to work abroad for about 15 years. Once I return to India, I may continue to work for a few more years. My son is one. My mother is dependent on me, but not financially. For all my goals, I save in RDs and from there I shift the proceeds to other investments. I am an aggressive investor.

— Gireesh

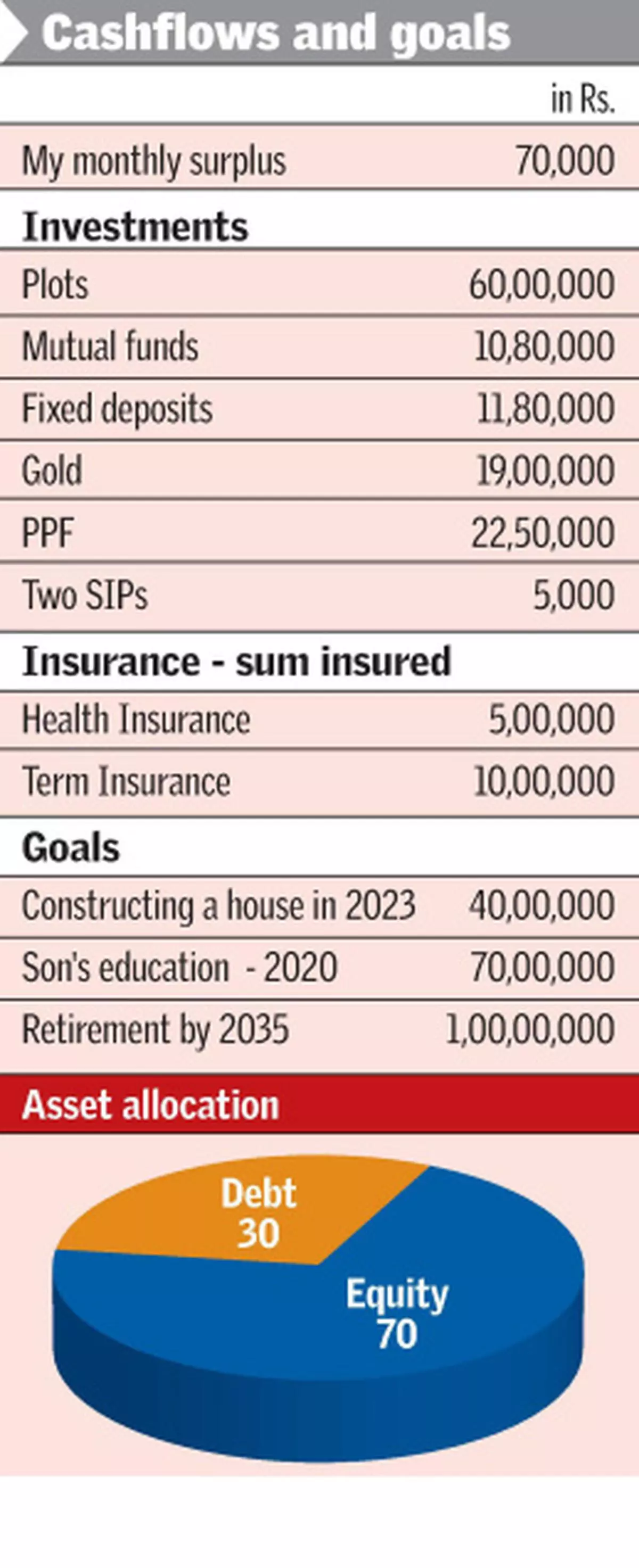

Asset allocation should be based on the risk profile and tenure of the goals. Although you have indicated that you are an aggressive investor, it is not reflected in your investments as real estate and debt investments account for more than 90 per cent of your portfolio.

While investing in equity mutual funds, you must opt for a systematic investment plan rather than putting in lump-sums in such schemes.

Given your monthly surplus, you can reach all your goals provided you work till the age of 55.

Son’s education

If you earmark your fixed deposits and PPF investments for this goal, you can reach 95 per cent of the target value. The rest can easily be met with your cash surplus during the respective years.

If you deploy your fixed deposits at a post-tax return of eight per cent, it will amount to Rs 20.2 lakh in 2020. Similarly, if your PPF investment continues to deliver 8.5 per cent, in the target year it will add up to Rs 39.82 lakh. If you continue SIP investments of Rs 5,000 and if it earns 12 per cent, you will be able to accumulate Rs 6.5 lakh. You will have a shortfall of Rs 3.5 lakh, which would quite easily be bridged.

Construction

The present cost of construction of Rs 40 lakh, if inflated at 8 per cent, will become Rs 86.35 lakh after 10 years. If you wish to retain the other plot for future construction purposes, you need to save Rs 37,540 every month for the next 10 years and it should earn 12 per cent returns.

Retirement

While living in India, if you currently incur annual expenses of Rs 3 lakh, then at 55, when you retire, you will need 13.3 lakh, if the inflation rate is 7 per cent.

To earn such an income till you turn 80, you should have a corpus of Rs 2.92 crore at retirement and it should earn a return of one per cent over and above inflation.

If you earmark your current investment in mutual funds for this purpose and if it earns 12 per cent you will have a corpus of Rs 58.71 lakh. To accumulate the balance, you ought to save a sum of Rs 18,240 per month for the next 22 years and it should earn 12 per cent returns.

But going through your mutual fund portfolio, it appears that you try to time the market. Even if you do time the entry and exit, such investments must not account for more than 5-10 per cent of your portfolio. Conduct a portfolio review at least once every quarter.

(The author is a practising chartered accountant)

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.