I am 56 and have taken voluntary retirement from service. My wife is a home maker aged 50. My daughter is studying in the US and will complete her course in 2015.

I have a medical insurance policy for Rs 1.25 lakh and company-sponsored health cover for Rs 1.25 lakh.

I plan to take an education loan for my daughter’s studies, but she will repay the debt.

I am suffering from asthma. After my daughter’s marriage, my monthly expenses will be Rs 35,000.

How can I reach my goals and live peacefully with our investments?

- Ramachandran

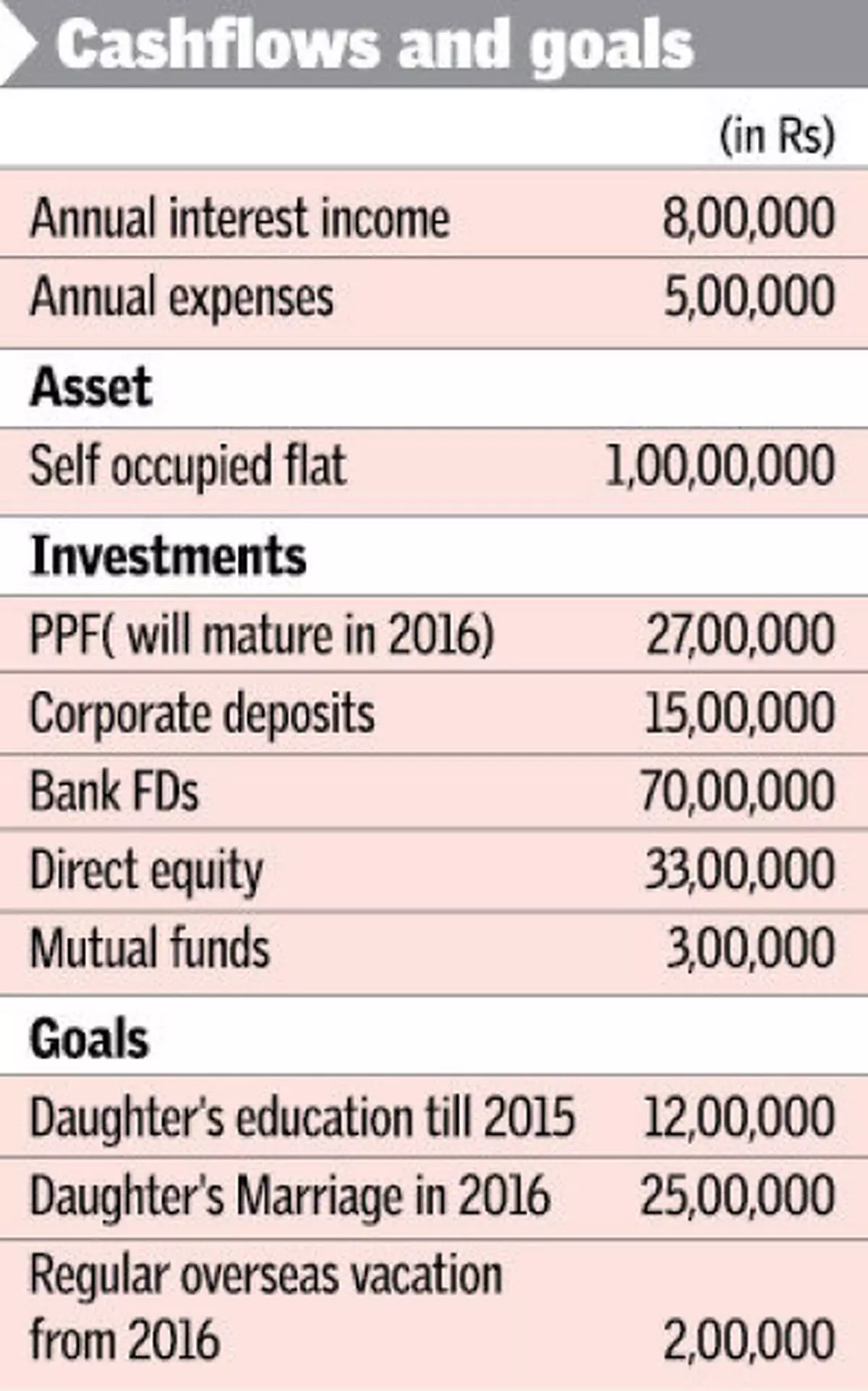

Since you have constructed a portfolio over the years, you can reach most of the goals. What you need to do is to reinvest monthly surplus to meet retirement goals.

The current income from your fixed deposits appears healthy. But if the inflation rate is 7 per cent, monthly expenses of Rs 35,000 will be Rs 74,000 when your are 70. From there on the shortfall will increase and at 80 your monthly expenses will be Rs 1.44 lakh.

If you continue to hold quality large-cap stocks in your equity portfolio over the next 10 years and even if your portfolio delivers conservative return of 10 per cent, it will take care of any shortfall.

Daughter’s education

If your daughter takes up employment post her education, she can comfortably repay the loan. Since you wish to perform her marriage immediately, she may not be in a position to close the loan before her marriage.

If she doesn’t seek employment after marriage, then repaying the loan will be a difficult task.

If the equity market delivers abnormal returns within the next few years, book profits beyond, say, 10 per cent gains, and set this amount aside as a separate fund to cover the repayment of the education loan. Otherwise utilise your corporate deposits to pre-close the loan.

Marriage

Since your PPF is maturing in 2016, it will take care of the expenses. Do earmark the surplus of Rs 2 lakh for post marriage expenses.

Vacation

After your daughter’s marriage, your expenses will reduce by 30 per cent. This will increase your surplus. . Utilise the same for your vacations till you turn 64.

Health insurance

The current coverage is low. It is advisable to increase your cover by another Rs 4 lakh to protect the retirement corpus.

Investment strategy

Although you have been investing in equities for the past 25 years, it is advisable to reduce the holding when you turn 70. If the equity portfolio delivers 10 per cent for next 13 years, your portfolio value will be Rs 1.13 crore. Move the proceeds to equity mutual funds or shift to debt funds if you want lower risks.Write a will for a smooth transition of your assets.

Mail your queries to >fp@thehindu.co.in

(The author is CEO, myassetsconsolidation.com)

![]() Comments

Comments

Comments

Comments have to be in English, and in full sentences. They cannot be abusive or personal. Please abide by our community guidelines for posting your comments.

We have migrated to a new commenting platform. If you are already a registered user of TheHindu Businessline and logged in, you may continue to engage with our articles. If you do not have an account please register and login to post comments. Users can access their older comments by logging into their accounts on Vuukle.